Identifying and Managing Risks - Business Decision Making - ثاني ثانوي

Part 1

Chapter1: Identifying and Defining Problems

Chapter2: Solving the Problem

Chapter3: Thinking Critically

Chapter4: Group Decision Making and Problem Solving

Chapter5: Decision Support Tools

Chapter 6: Decision-Making Processes in Organizations

Chapter 7: Managing Teams to Support Decisions in Organizations

Chapter 8: Organizational Communication and Decision Making

Part 2

Chapter 9: Using Data to Support the Decision-making Process

Chapter 10: Decision Support System Fundamentals

Chapter 11: Using Microsoft Excel Solver

Chapter 12: The Car Production Project

Chapter 13: The Ski Resort Project

Chapter 14: The Electric Car Project

Chapter 15: The Airline Project

Part 1

Chapter1: Identifying and Defining Problems

Chapter2: Solving the Problem

Chapter3: Thinking Critically

Chapter4: Group Decision Making and Problem Solving

Chapter5: Decision Support Tools

Chapter 6: Decision-Making Processes in Organizations

Chapter 7: Managing Teams to Support Decisions in Organizations

Chapter 8: Organizational Communication and Decision Making

Part 2

Chapter 9: Using Data to Support the Decision-making Process

Chapter 10: Decision Support System Fundamentals

Chapter 11: Using Microsoft Excel Solver

Chapter 12: The Car Production Project

Chapter 13: The Ski Resort Project

Chapter 14: The Electric Car Project

Chapter 15: The Airline Project

Lesson 4 Chapter 1 Identifying and Managing Risks Any decision you make or solution you implement involves some risk, which is an exposure to a chance of loss or damage. Although the solution you develop might succeed or fail, you are risking time, money, and effort with each decision you make. Risk is an inevitable part of business, especially when you are intro- ducing creative changes. With careful planning, you can often avoid many of these risks or reduce their drawbacks. If the potential risk is significant enough, you might need to take a different approach altogether (which is called risk avoidance). case One of the smaller problems you identified for the travel company you're working at involves tour frequency-customers would like to take popular tours more often. Omar encourages you to identify the risks associ- ated with this problem and solution before introducing it to managers at the company. DEFINITION Risk: An exposure to a chance of loss or damage. TABLE 1-4: Problem risks do's and don'ts Elements Risk Testing Do Identify all risks before making a decision. Identify the costs of each risk Recognize the potential rewards • Seek solutions that are low risk and high reward • Try out a solution on a limited basis • Make sure a test reveals strengths and weaknesses • Communicate the results of the test to everyone involved Don't • Don't disregard the consequences of taking a risk • Don't minimize the risk or the reward • Don't choose solutions that are high risk and low reward •Don't ignore unpopular or unwelcome test results • Don't forget to test your backup plan of a solution. • Don't avoid communicating bad news 34 Chapter 1 Ministry of Education 2024-1446 Essential Elements 1. Be aware of potential risks As you consider alternatives and possible solutions, ask what might go wrong with each. What is the likelihood that a particular solution will succeed or fail? What would the costs be if a solution didn't work out? Would failure complicate the problem further, or could you easily try a different solution? Consider the answers to these questions when making decisions and assess- ing your options. 95198_book_PP1.indb 34 07/05/2024 10:57

Identifying and Managing Risks

Problem risks do’s and don’ts

Essential Elements: Be aware of potential risks

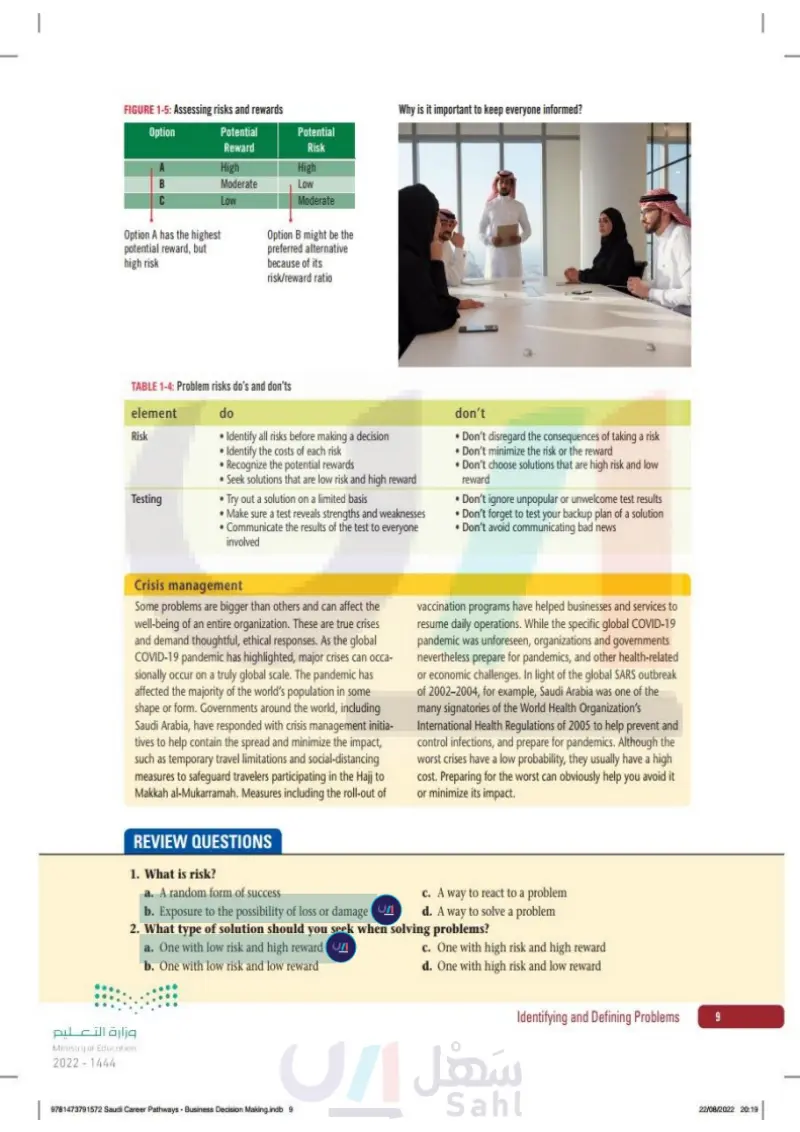

2. Assess your risk/reward ratio While risks are a part of any decision you make, rewards are associated with successful problem solutions. Consider both outcomes. Avoid solutions that carry significant risk, but minimal reward. If your recommended solution does not solve the main problem, much of the cost will come at the expense of your credibility. Solutions that are low risk and high reward are ideal. See Figure 1-5. FIGURE 1-5: Assessing risks and rewards Option Potential Potential Reward Risk A High High B Moderate Low C Low Moderate QUICK TIP Be sure to communicate your plans to others who may be affected or whose help you will need. Option A has the highest potential reward, but high risk Option B might be the preferred alternative because of its risk/reward ratio 3. Reduce your risk by testing Testing a solution involves trying it on a small or limited basis. A well-de- signed test shows the strengths and weaknesses of an idea while limiting your exposure and expense. If the test is unsuccessful, you can try another alternative with minimal cost. When your tests are successful, they often give you insight into ways you can refine and improve your solution before you implement it on a wider scale. For example, the travel company you're work- ing at could reduce its tour costs by switching to a no-frills airline. However, your customers might react negatively to the change. You could test this solution by using a low-cost carrier for a few select tours and then carefully surveying your clients about their perceptions. 4. Develop a fall-back position or a backup plan Sometimes even well-conceived ideas fail. What will you do in response? The point of failure is a poor time to begin considering alternatives. The greater the potential effect of your decision, the more important it is to have a backup plan in place. 5. Keep everyone informed Being surprised by something going wrong is often worse than the draw- back itself. Avoid surprising your supervisor, problem owner, and other stake- holders by something you do. Keep them informed and communicate your وزارة التعليم Ministry of Education 2024-1446 Business Decision Making S1 S2 S3.indb 35 Identifying and Defining Problems 35 30/06/2023 14:27

Assess your risk/reward ratio

Reduce your risk by testing

Develop a fall-back position or a backup plan

Keep everyone informed

Why is it important to keep everyone informed? intentions and actions. They can sometimes see a problem before it happens and provide you with an early warning. If something does go wrong, keep- ing them in the loop will help to reduce the damage. Crisis management Some problems are bigger than others and can affect the well-being of an entire organization. These are true crises and demand thoughtful, ethical responses. As the global COVID-19 pandemic has highlighted, major crises can occasionally occur on a truly global scale. The pandemic has affected the majority of the world's population in some shape or form. Governments around the world, including Saudi Arabia, have responded with crisis management initiatives to help contain the spread and minimize the impact, such as temporary travel limitations and social-distancing measures to safeguard travelers participating in the Hajj to Makkah al-Mukarramah. Measures including the roll-out of vaccination programs have helped businesses and services to resume daily operations. While the specific global COVID-19 pandemic was unforeseen, organizations and governments nevertheless prepare for pandemics, and other health- related or economic challenges. In light of the global SARS outbreak of 2002-2004, for example, Saudi Arabia was one of the many signatories of the World. Health Organization's International Health Regulations of 2005 to help prevent and control infections, and prepare for pandemics. Although the worst crises have a low probability, they usually have a high cost. Preparing for the worst can obviously help you avoid it or minimize its impact. 36 Chapter 1 Ministry of Education 2024-1446 Business Decision Making S1 S2 S3.indb 36 30/06/2023 14:27

intentions and actions. They can sometimes see

Crisis management

YOU TRY IT Practice identifying and managing risks by ranking possible solutions to a prob- lem. Complete the following steps. 1. Get ready Read the following description of a problem. Problem: Sales at the travel company so far this year are weak. What can the company do to increase sales? 2. Now you try it In your notebook, or using a word processor, complete the following risk/ reward table to score each solution according to the risks and rewards it presents. Assign a score of High, Moderate, or Low to each option. Identify the preferred alternative. Option Potential Reward Potential Risk Increase tour prices Offer popular tours more often REVIEW QUESTIONS Cut expenses, including staff Explain why you assigned the scores you did. 1. What is risk? a. A random form of success b. Exposure to the possibility of loss or damage c. A way to react to a problem d. A way to solve a problem 2. What type of solution should you seek when solving problems? a. One with low risk and high reward b. One with low risk and low reward c. One with high risk and high reward d. One with high risk and low reward وزارة التعليم Ministry of Education 2024-1446 Business Decision Making S1 S2 S3.indb 37 Identifying and Defining Problems 37 30/06/2023 14:27

Complete the following steps. Get ready Read the following description of a problem

What is risk?

What type of solution should you seek when solving problems?